A CPG data brief on what separates early traction from retail entry, and what closes it.

Estimated reading time: 13 minutes

She has a product that sells. She has customers who come back. She has been running her business for more than a year, managing suppliers, filling orders, and reinvesting what she earns. For a founder reporting household income below $75,000, reaching retail is not just a business milestone. It is the kind of economic shift that creates jobs, builds community wealth, and changes what is possible for her family.

The programs designed to close that distance would, by their own eligibility criteria, turn her away.

She is not an edge case. She is the median founder in SEED SPOT’s applicant pool, and her situation is the reason we built the Retail Brand Accelerator and the reason we are sharing this data. What follows is what we learned about the gap she is navigating and what actually closes it.

Finding 1: The founders who need retail support most can’t qualify for it.

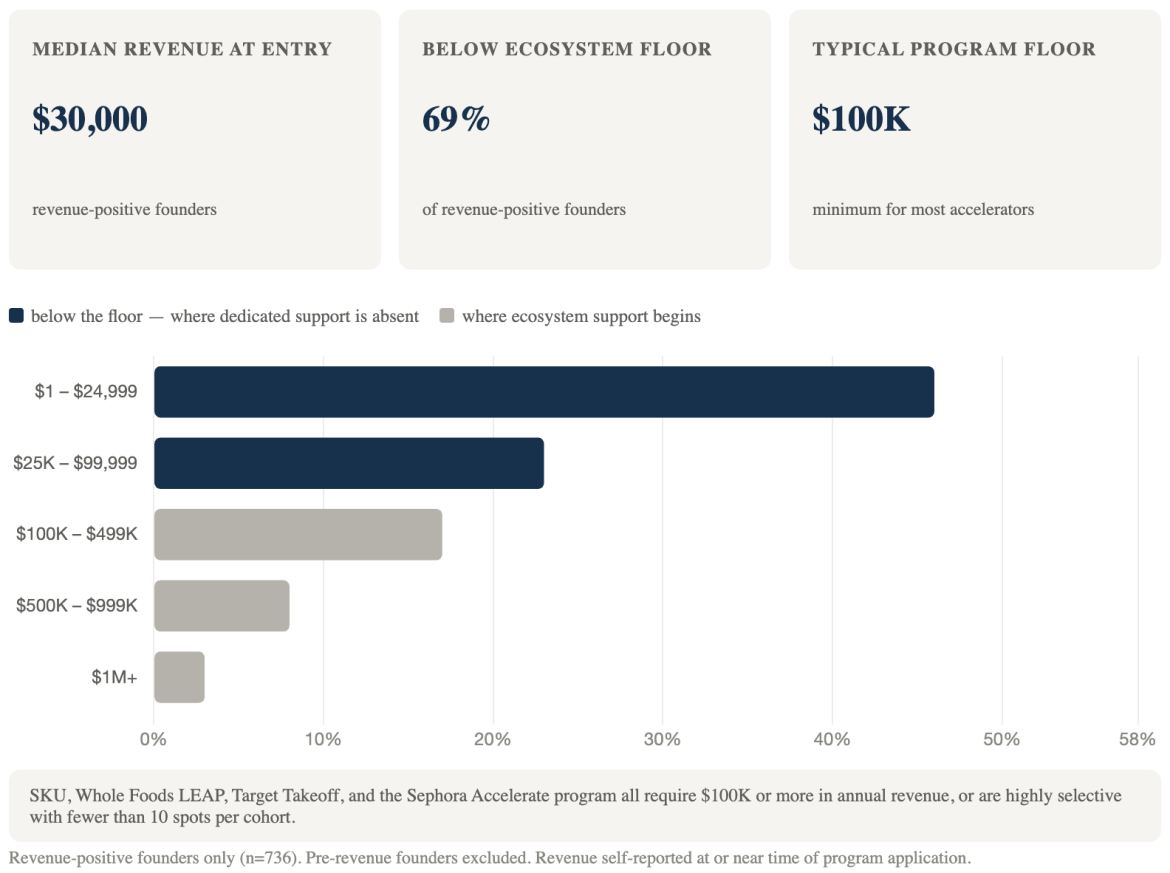

Among revenue-positive CPG founders in SEED SPOT’s pipeline, the median annual revenue at application is $30,000. For a founder at that stage, a single purchase order from a regional retailer can represent more revenue than everything she generated the year before. That is not a marginal improvement in her business. It is a structural shift in what kind of business she has, and it is exactly the kind of shift our founders are making.

The mean annual revenue across the same dataset is $687,000, a figure that sounds encouraging until you understand what is driving it. A small number of high-revenue outliers account for nearly 70% of all revenue in the pool. When extreme values pull an average that far from the center of a distribution, the average stops describing a typical experience. The $30,000 median is the operative figure, and it sits well below the threshold at which the ecosystem begins to serve it.

The major retail-facing accelerator programs in the United States cluster around a common eligibility floor of $100,000 in annual revenue. SKU, the most widely cited independent CPG accelerator nationally, requires $100,000 or more. Whole Foods’ LEAP Early Growth cohort received more than 1,600 applications for 10 spots in 2025. Target Takeoff targets brands preparing for mass retail scale. The Sephora Accelerate program is beauty-only and selects approximately eight brands per year from a pool of hundreds. Below that floor, what exists tends to be geographically constrained, category-specific, or oriented toward general business development rather than retail entry.

Sixty-nine percent of revenue-positive founders in SEED SPOT’s pipeline fall below that floor. They are not unaware of what they need. Sixty-one percent named retail access as their primary goal at program entry. What the ecosystem has not provided is a structured path to get there.

The $100,000 floor carries an assumption worth examining: that a viable path to that threshold exists outside of retail. For founders building through direct-to-consumer channels without access to capital, industry networks, or wholesale relationships, that assumption does not hold. The channels available at the $30,000 stage — local markets, online storefronts, farmers markets — generate real traction but have real ceilings. The volume, reorder frequency, and distribution reach that compound revenue toward $100,000 and beyond is precisely what retail provides. For many of these founders, retail is not the destination after $100,000. It is the route there. A floor designed to ensure brands are ready for retail may, in practice, exclude the founders for whom retail is the mechanism of getting ready.

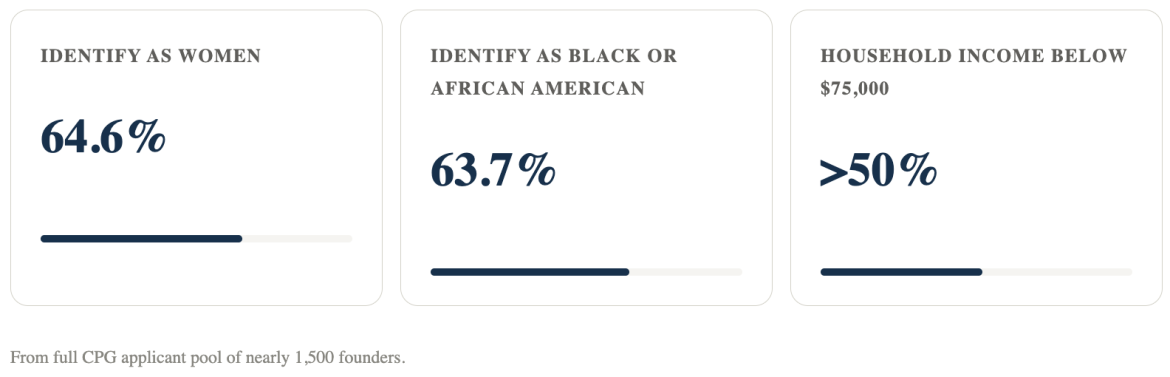

That gap is not randomly distributed across the founder population. Across nearly 1,500 CPG founders in SEED SPOT’s pipeline, 64.6% identify as women and 63.7% identify as Black or African American. More than half report household incomes below $75,000. The networks, mentorship relationships, and industry exposure through which retail knowledge has historically been transmitted have not been equally available to all founders. The ecosystem floor of $100,000 does not just describe a revenue threshold. It describes, in practice, a proximity threshold: how close a founder already is to the retail world before she applies.

Finding 2: Five knowledge areas separate founders from pitch readiness.

When a retail buyer sits down with a founder for a first pitch conversation, she arrives with a set of assumptions. She assumes the founder knows how to present her product in a format buyers can evaluate. She assumes the founder understands the economics of a retail relationship. She assumes the founder can articulate how her product gets from production to shelf. These assumptions are reasonable in the context of brands that have been in retail conversations before. They are almost universally wrong for founders entering retail for the first time.

A founder who has spent two years selling at farmers markets and through her own website has learned real things: how to talk to customers, how to price for direct margin, how to build a following. Those channels reward the skills she has developed. They do not reward, and do not require, the skills a retail buyer will ask about in the first five minutes of a pitch conversation. Capital and customer reach feel like the constraints because they are the constraints those channels surface. The operational requirements of retail are invisible from inside a business model that has never needed them. The perceived gap and the actual gap are different gaps, and the distance between them is not a failure of awareness. It is a structural feature of building a business in channels that were never designed to prepare a founder for retail.

SEED SPOT’s program data identifies five discrete knowledge areas that separate founders at the $30,000 stage from pitch readiness. Among retail-specific curriculum topics, these rated highest in post-session evaluations. Together they constitute not an advanced curriculum but an entry-level foundation — the baseline a buyer assumes is already in place. None of them appeared in the top stated needs of founders entering the program. All of them were rated among the most valuable sessions once founders encountered them.

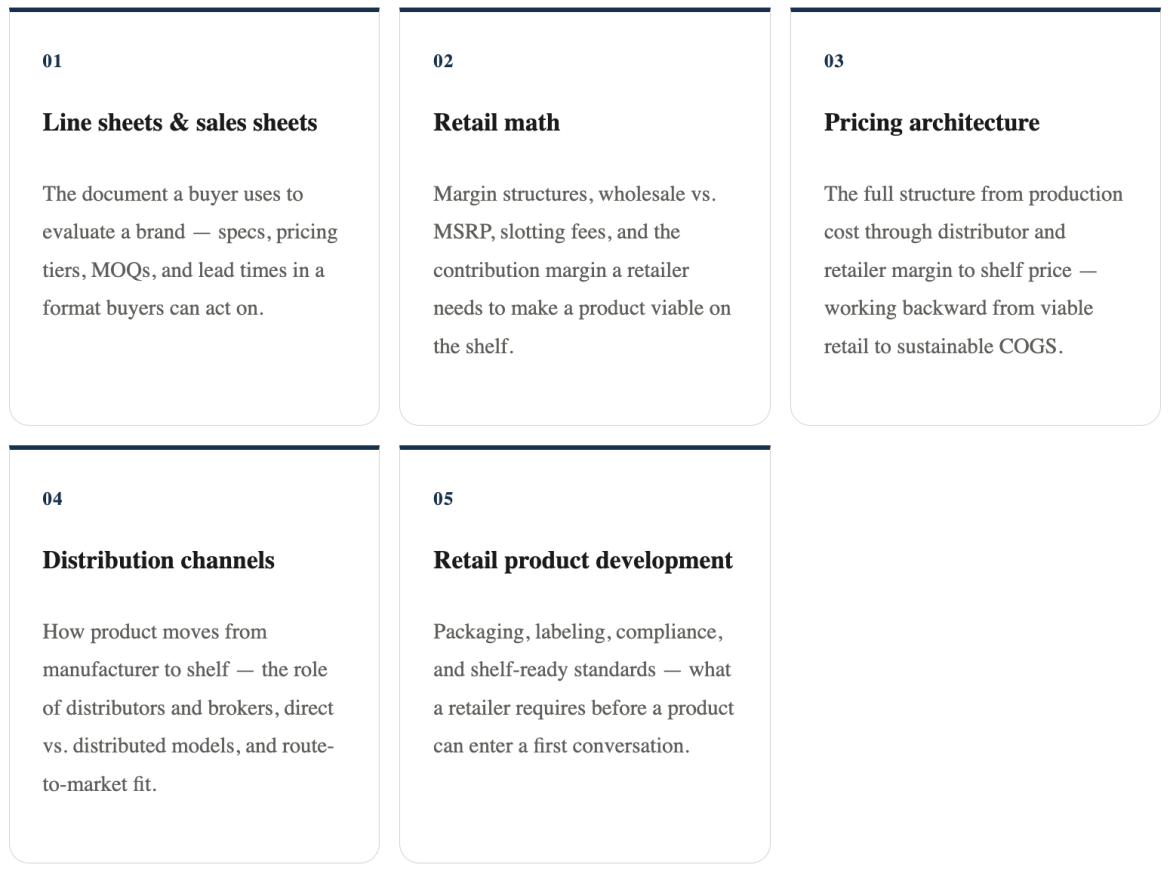

Line sheets and sales sheets. The line sheet is the document a buyer uses to evaluate a brand. It presents product specifications, pricing tiers, minimum order quantities, and lead times in a standardized format that allows a buyer to assess viability without asking for basic information the founder should already have organized. Most founders at program entry have never built one. Buyer feedback from RBA pitch sessions confirmed that line sheet readiness is among the most critical factors determining whether a buyer conversation can move forward at all.

Retail math. Retail math is the economic language of a vendor relationship. It covers margin structures, cost of goods calculations, wholesale versus MSRP pricing, slotting and promotional fees, and the contribution margin a retailer needs to make a product viable on the shelf. A founder who does not understand retail math cannot tell a buyer whether her product is financially viable for the retailer’s category. Buyers noted in their feedback that when pricing information was absent or unclear, they were left guessing at margin, which in practice means the conversation ends. The math is not complicated. It is simply not taught in the channels founders have been building in. Cash flow confidence was the lowest-rated self-efficacy dimension founders reported at program entry and showed the largest gain by program exit, a shift consistent with what founders report gaining from this curriculum area.

Pricing architecture. Consumer-facing pricing and retail pricing are different problems. Pricing architecture covers the full structure from production cost through distributor and retailer margin to shelf price, and requires a founder to work backward from a viable retail price to a cost of goods that makes the margin stack work at every point in the chain. Founders who have built their businesses through direct-to-consumer channels have typically priced for a different margin structure entirely, one that collapses when a distributor and a retailer each need to take their margin before the product reaches a shelf.

Distribution channels. Understanding how product moves from manufacturer to shelf, the role of distributors and brokers in that chain, the difference between direct-to-retail and distributed models, and how to identify the right route to market for a given retailer type is foundational knowledge for any retail conversation. A buyer evaluating a brand needs to know the founder has thought through logistics, compliance, and channel fit before committing to a relationship. It is also knowledge that is entirely invisible from inside a direct-to-consumer or farmers market business model, where the founder is the distributor.

Retail product development. What a product needs to look like, how it needs to be packaged, what labeling and compliance requirements apply, and what shelf-ready means in the context of a specific retailer are not universal standards. They vary by channel, category, and retailer, and they represent a set of requirements a buyer will raise in a first conversation that a founder without retail experience will not anticipate. Buyers in SEED SPOT’s pitch sessions offered channel-specific guidance on shelf stability, ingredient compliance, and distributor readiness that founders described as information they had no prior access to.

These five areas are not advanced concepts. They are entry-level requirements, the baseline a buyer assumes is in place before a conversation is worth having. The founders in SEED SPOT’s pipeline are not lacking in ambition, product quality, or customer validation. They are lacking exposure to a body of knowledge that has historically been transmitted through broker relationships, industry networks, and retail experience that this population has not had access to.

Buyer evaluations from RBA pitch sessions confirm independently what these founders need. Across evaluations from buyers at Macy’s, Walmart, Whole Foods, and independent grocery and beauty channels, buyer qualitative feedback named line sheets, pricing structures, and retail-specific materials as the factors that determine whether a conversation moves forward. When those elements were in place, buyers responded: 86% indicated they wanted to follow up after the session, with specific next steps documented including introductions to category teams and invitations to resubmit after compliance review.

Finding 3: These founders, equipped with training, win meetings and PO’s.

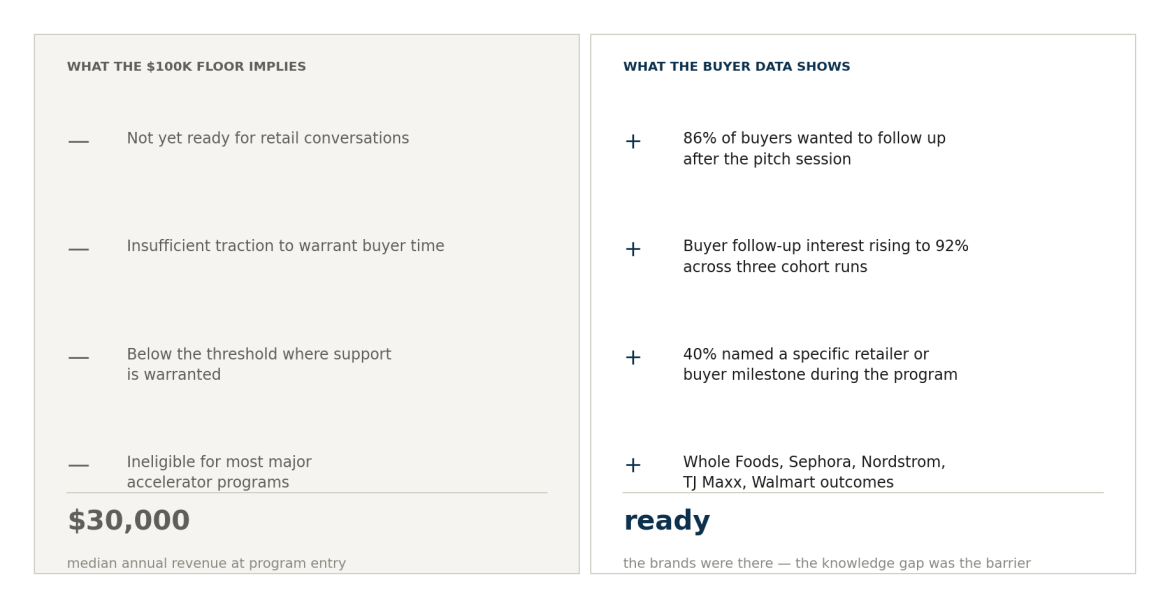

The ecosystem’s $100,000 revenue floor implies that founders below it are not yet ready for retail. The buyer and outcome data from the Retail Brand Accelerator says otherwise.

When founders arrived at buyer pitch sessions equipped with the five knowledge areas, 86% of buyers indicated they wanted to follow up after the session. Among founders who scored highest in buyer evaluations, that figure rose to 93%. Across three cohort runs from 2024 to 2025, buyer follow-up interest rose from 71% to 90% to 92%, and the proportion of evaluations containing strongly positive language rose from 43% to 62%. These are not outcomes from founders who cleared the ecosystem’s $100,000 threshold. They are outcomes from founders whose median annual revenue at program entry was $30,000.

Forty percent of post-program participants named a specific retailer, buyer meeting, or retail milestone they achieved during the program. Outcomes included a Whole Foods launch, a Sephora buyer conversation, a Nordstrom placement for Black Business Month, a TJ Maxx buyer meeting, and a Walmart buyer conversation, among others. Eighty-one percent of post-program participants reported being extremely satisfied with the program. The net promoter score was 80.

For a founder whose annual revenue is $30,000, any one of those outcomes represents a structural shift in what kind of business she has. The leverage point is not the retail placement itself. It is pitch readiness, which is a much smaller and more tractable problem than it appears from the outside. Five teachable knowledge areas, a structured program environment, and access to real buyers produce a measurable change in what is possible for these founders within the program window. The revenue entry point is not a ceiling. It is a starting line, and the data shows where it leads.

The founder in the opening of this brief, the one the programs would turn away, is the same founder who leaves with a line sheet, a retail math model, and a buyer who wants to talk. That is not the end of the story. It is the beginning of it.

Takeaways

For philanthropic funders. The knowledge gap is discrete, teachable, and documented with specificity. Founders entering at $30,000 in annual revenue are producing buyer follow-up rates of 86% and named retail outcomes at 40% within an eight-week window. The intervention is defined, the population is large, and the outcomes are measurable. What the field needs now is more programs built specifically for this stage. If you fund entrepreneurship support, retail readiness for founders below the ecosystem’s floor is one of the highest-return, most underinvested opportunities available. We are building that infrastructure at SEED SPOT, and we are looking for partners who want to scale it.

For retailers. When founders arrive prepared, buyers want to continue the conversation. The 86% follow-up rate is not a program outcome. It is a market signal: there is a pipeline of compelling, underreached brands at the $30,000 stage that the ecosystem has not surfaced to you yet. Participating in buyer pitch sessions is one of the most direct ways a retail organization can access that pipeline, support the founders who are building toward your shelves, and shape what retail-ready looks like for the next generation of brands. If you are interested in bringing buyers into the RBA or exploring a partnership, we would like to hear from you.

For peer organizations. The $30,000 median likely describes a large and poorly documented population of operating CPG founders across the country navigating a gap the field has not yet organized around. The assumption embedded in the $100,000 floor, that there is a viable path to that threshold outside of retail, does not hold for founders building without access to capital, industry networks, or wholesale relationships. If your program serves founders at an adjacent stage, the founders you are graduating may be exactly who the Retail Brand Accelerator is built for next. We are actively looking for referral partners and peer organizations who want to build the connective tissue that keeps founders moving forward. If that sounds like your work, we would like to connect.

For founders. If you are generating revenue, have customers who return, and have been told you need more capital or a better marketing strategy before you can approach retail, the data suggests the diagnosis may be incomplete. The gap between where you are and a buyer follow-up conversation is likely not capital or marketing. It is five specific, learnable knowledge areas: line sheets, retail math, pricing architecture, distribution channels, and retail product development. None of them requires prior retail experience or broker relationships. They require the right program at the right stage. If you are building a CPG business at the $30,000 stage and retail feels like the next frontier, the Retail Brand Accelerator was built for exactly where you are. We would love to see your application.

Download the checklist to score your readiness here

SEED SPOT is a national entrepreneurship nonprofit that educates, accelerates, and invests in impact-driven founders. Learn more about the Retail Brand Accelerator at seedspot.org.

This brief draws on records from nearly 1,500 CPG founders in SEED SPOT’s programs and pipeline, post-session evaluations from the Retail Brand Accelerator, and buyer feedback from RBA pitch sessions from 2024 to 2025. Demographic data draws on SEED SPOT program application records.

Learn more about the Retail Brand Accelerator: seedspot.org/seed-spot-retail-accelerator